When people think about retirement planning, they naturally focus on their investments. After all, your portfolio is often expected to replace the paycheck you’ve relied upon for decades.

But there is another factor that can have a significant impact on your long-term financial outcomes—how you pay for advice or management.

For years, the wealth management industry has largely relied on a single pricing model: charging a percentage of assets under management, commonly known as an AUM fee. Because the fee is deducted directly from investment accounts, many investors rarely stop to evaluate whether the amount they’re paying reflects the value they’re receiving.

As retirement approaches, that question becomes increasingly important. The goal isn’t simply to minimize fees. It’s to understand what you’re paying for, how your advisor is compensated, and whether the services being provided justify the cost.

Investors may want to ask a simple question:

Does the amount I pay accurately reflect the value I receive?

Why Most Investors Focus on Returns and Ignore Fees

Turn on any financial news network, and the headlines are relentlessly focused on one thing: performance. The industry conditions us to constantly track macro trends—whether that means bracing for stagflation, analyzing Federal Reserve interest rate shifts, or watching how geopolitical conflicts impact global markets.

It is entirely natural to obsess over asset allocation and chase the highest possible returns. Focusing on the market feels like you are actively steering the engine of your wealth creation. But this hyper-focus on performance creates a massive psychological blind spot when it comes to the true cost of investing.

Here is why fees are overlooked:

- The frictionless payment: One reason advisory fees receive less scrutiny than other expenses is that they are typically deducted directly from investment accounts rather than paid through a separate invoice. When you pay a 1% AUM fee, you rarely write a physical check. Because the fee is often deducted automatically, many investors never experience the same psychological awareness they would if they were writing a check each quarter.

- The pennies fallacy: Human brains are not wired to intuitively understand the math of compound degradation. A 1% fee sounds small; it feels equivalent to a tiny sales tax. We fail to recognize that surrendering 1% of our entire net worth every single year is fundamentally different from a one-time transaction cost.

- The Asymmetry of Control: Investors spend endless hours analyzing market returns because they want to feel in control of their financial destiny. The irony is that market performance is entirely out of your hands. You cannot control the S&P 500, and you cannot control global economic policy. But you can control exactly how many of your dollars are surrendered to advisory fees.

This doesn’t mean advisory fees are inherently excessive or unjustified. Many advisors deliver substantial value through retirement planning, tax planning, and behavioral coaching – not just investment management.

The problem is that investors often scrutinize investment performance far more closely than they scrutinize the cost of obtaining advice.

Before determining whether a fee is reasonable, investors should first understand how the fee is calculated and what services they are actually receiving in return.

The 1% Industry Standard

For decades, the wealth management industry has largely relied on a simple pricing model: charging a percentage of the assets being managed, commonly referred to as an Assets Under Management (AUM) fee. While fee schedules vary, 1% has long been viewed as a common benchmark for many advisory relationships.

The appeal of the model is straightforward. As a client’s portfolio grows, the advisor’s compensation grows as well. In theory, both parties benefit from the same objective: increasing the value of the portfolio over time. For many advisors and clients, this arrangement has worked well and remains the dominant pricing structure today.

However, the financial planning profession has evolved significantly. Today’s retirees often need guidance that extends well beyond portfolio management, including retirement income planning, required minimum distribution (RMD) strategies, Social Security decisions, tax planning, Medicare considerations, and estate planning coordination. As a result, investors may want to ask a simple question: Is account size still the best way to determine the cost of financial advice?

The Math Behind Advisory Fees

Advisory fees are often discussed as percentages, but percentages can be deceiving.

A 1% annual fee may not seem significant in any single year. However, because the fee is charged against a growing portfolio, the long-term impact can become substantial.

This doesn’t mean an AUM fee is inherently bad. Many advisors provide value that far exceeds the fee they charge. But investors should understand how different compensation structures affect long-term outcomes.

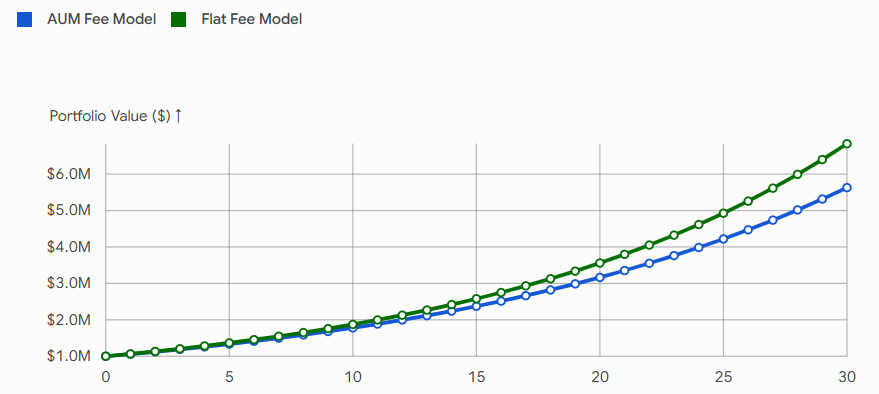

Consider a hypothetical investor with a $1 million portfolio earning an average annual return of 7% over 30 years.

Under a traditional 1% AUM arrangement, the advisory fee rises as the portfolio grows. Under a fixed-fee arrangement, the investor pays for the planning relationship itself rather than a percentage of assets.

The 30-Year Impact

| Compensation Model | Annual Cost (Year 1) | Total Wealth After 30 Years |

| 1% AUM Fee | $10,000 | $5,743,491 |

| Flat $6,000 Fee | $6,000 | $7,078,000 |

Note: The flat fee calculation assumes the $6,000 fee adjusts upward by 3% annually for inflation.

By transitioning from a 1% AUM fee to a flat fee structure, the portfolio retains over $1.3 million in additional wealth. You aren’t just saving on the fee itself; you are keeping the compound growth that those fee dollars would have earned over three decades.

The purpose of this comparison isn’t to suggest that one pricing model is universally better than another. Rather, it illustrates that fee structure can have a meaningful impact on long-term wealth accumulation.

Of course, cost is only one side of the equation.

The more important question is whether the advice being delivered justifies the fee being charged. If two investors each pay 1% annually, but one receives investment management alone while the other receives retirement income distribution planning and tax planning are they receiving the same value?

Fee-Based vs. Fee-Only: The Crucial Distinction

These terms sound nearly identical, but the difference in how they impact your portfolio is profound.

Fee-Based Planners

“Fee-based” simply means the advisor charges a fee (usually a percentage of your assets), but they are also legally allowed to accept commissions from third parties. This creates an inherent conflict of interest.

If an advisor is recommending a variable annuity, a front-loaded mutual fund, or a universal whole life insurance policy, you have to ask: Are they recommending this because it is the optimal solution (accounting for low to no additional charges), or because they receive a commission for selling it?

Fee-Only Planners

A fee-only planner is compensated entirely and exclusively by the client. They do not sell products, they do not accept kickbacks, and they do not receive commissions from brokerage firms.

Because the compensation is transparent and direct, the conflict of interest is removed. Whether we are modeling a dynamic withdrawal strategy using the Guyton-Klinger method or troubleshooting state-specific tax sourcing on corporate bonds, the advice is completely objective. The only incentive is to grow and protect your wealth.

The Bottom Line

Investors shouldn’t choose an advisor based solely on the fee structure.

They should understand what services are being delivered, how those services support their goals, and whether the advice addresses the increasingly interconnected decisions that come with retirement.

Some firms continue to charge based primarily on assets under management. Others utilize fixed-fee or subscription-based arrangements that attempt to align fees with the scope of planning being provided.

Neither approach is inherently right or wrong. The key is understanding what you’re paying for and whether the value delivered justifies the cost.

Ultimately, investors should focus less on finding the cheapest advisor and more on finding the right advisor—one who provides the level of guidance, expertise, and coordination needed to help them achieve their long-term goals.